Turtles are unique as they are amphibians (can live both in land and water). The ubiquitous turtle is seen in most shops and commercial spaces. It is popularly believed that it brings good fortune.

Here is some back story. Of the ten avatars of Vishnu, one of them was Koorma (turtle). It is believed that there was a power struggle between devas (good guys) and the asuras (bad guys) and it could be only solved by getting Amrit (nectar). To obtain Amrit, the ocean of milk had to be churned and they got a mountain named Mandara (to be used as a spindle) and a long snake named Vasuki (to be used like a rope). However, the spindle needs to rest on something which cannot be flat else the rotary action won’t be possible. This is when lord Vishnu took the avatar of a turtle and let Mandara rest on his back to facilitate the process. The Samudra Manthan led to all sorts of things coming out including the deadliest poison (halahal) and Amrit (sweetest nectar).

Let’s think of this in the context of market. What our investment team try, is to churn and get profit (amrit) while there could be unintended outcomes in form of losses. The bulls and bears spin Mandara (the markets) on either side producing all types of outcomes from big gains to massive pain! You get the drift of the story but what remains solid is the turtles back: strong and resilient! It remains at the centre while the bulls and bears fight it out.

The only amphibian in our business is long-short products which can hopefully do well in both good markets and not so good markets. Not surprisingly, they are called absolute return or market neutral strategies due to it market neutral positioning just like the turtle at the centre.

The strong shell-like back gives it resilience and behaves like a shield to keep the turtle out of harm’s way. the soft body gives it the ability to move on land and water. Similarly, the shorts act like the back shield while the longs run to seek alpha.

Let’s see how the funds have done..

Slow and steady wins the race: TEPA (Tata Equity Plus Absolute Returns Fund) has delivered 7.3% gross return FYTD till Dec 31st and Nifty 50 has delivered 5.9%, thereby outperforming by 1.4%. This should remind you of the hare and tortoise story. Reminds me of the tagline of one of the toothpastes which says “Mazedaar nahi, asardaar”. Objective of any investment is not fun/thrill but returns. TARF (Tata Absolute Return Fund) did a similar act with 7.6% gross return for 9 months vs its benchmark (CRISIL MT Debt Index) return of 5.9%.

When there is nothing intelligent to do, the mistake is often trying to be intelligent – The funds have been able to hide under the hard shell and reduce net exposure when markets appeared expensive and fundamentally disconnected. This is evidenced by reduction in net exposure in the funds which helped in avoiding unnecessary risk. We kept net equity low in H1FY25 since valuations were expensive, and slowly started dialling up as markets corrected.

Moving slowly into low-risk opportunities – the funds were able to capture opportunities in IPOs and QIPs which were relatively low risk and added to alpha. Risk rewards looked favourable in these and led to better returns. Close to 1% return were contributed by these opportunities in both the funds over the last quarter.

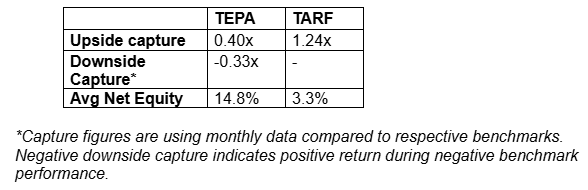

Stillness > Striving – The funds were able to hold steady and still rather than trying to get desperate and strive. This led to much lower drawdown thereby better performance even while equity performance was negative in certain months. This is evidenced by months like December when Nifty 50 was down while TEPA was positive, and when Nifty was down over 6% in October, the fund had a minimal drawdown.