Albert Einstein once famously said, “Compounding is the eighth wonder of the world.” While we often hear about the power of compounding in financial discussions, consistently compounding wealth remains the key to achieving true financial freedom. But how can investors construct a portfolio that grows wealth steadily while minimizing risk? The answer lies in multi-factor investing strategies. Let’s explore how data-driven factor investing can help create a resilient and high-performing portfolio.

Factor Investing: A Smarter Approach to Portfolio Construction

Factor investing, also known as smart beta or factor-based investing, involves constructing portfolios based on certain characteristics or factors historically linked to superior risk-adjusted returns. These factors go beyond traditional market beta and provide a systematic way to capture excess returns.

Common Factor Investing Strategies:

- Value Investing: Selecting stocks that trade at a lower price relative to their fundamental value.

- Quality Investing: Investing in companies with strong financials, low debt, and sustainable earnings.

- Momentum Investing: Investing in stocks that have shown recent price strength.

- Low Volatility Investing: Selecting stocks with lower historical price fluctuations.

- Small-Cap Investing: Focusing on smaller market capitalization stocks with high growth potential.

Each of these factors has historically demonstrated the ability to enhance portfolio returns and reduce risk.

Applying Factor Investing to Build a Stock Portfolio

Factor investing enables investors to systematically build stock portfolios based on their financial goals and market conditions. The steps to constructing a factor-based portfolio include:

- Define Investment Goals – Are you aiming for long-term growth, income, or stability?

- Select Factors – Choose relevant factors based on market conditions and risk appetite.

- Screen and Select Stocks – Identify stocks that exhibit strong factor characteristics.

- Diversify Across Sectors – Reduce exposure to specific industries to mitigate risk.

- Allocate Capital Strategically – Use equal weighting or factor weighting to optimize performance.

- Monitor and Rebalance – Regularly review portfolio performance and make tactical adjustments.

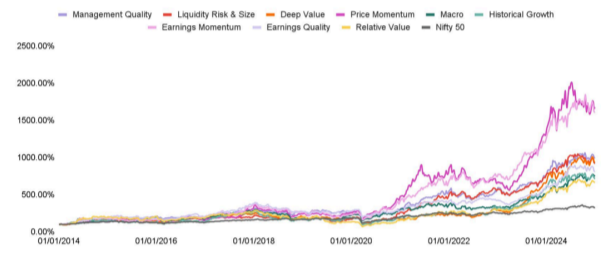

Performance of Factor-Based Investing in India

At Wright, we leverage proprietary models to construct factor portfolios. Our multi-factor strategies have consistently outperformed market benchmarks, delivering up to 35%+ CAGR over the last decade on a backtested basis. Among the leading factors, momentum, quality, and low volatility have generated the highest returns.

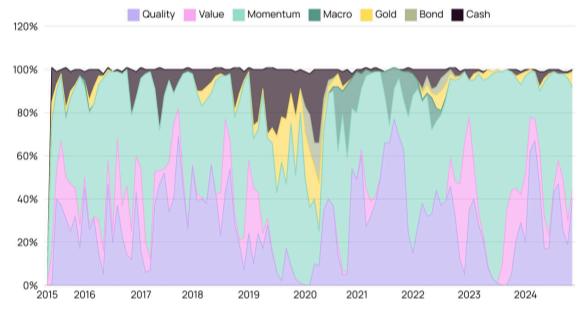

Tactical Factor Allocation: A Dynamic Approach to Investing

Just as different economic cycles favor specific asset classes, factor performances also vary across market cycles.

- Early Growth Phase: Momentum and Small-Cap factors tend to outperform.

- Slow Growth Phase: Quality stocks become more attractive.

- Late Cycle: Low Volatility strategies help mitigate risks.

- Recessionary Phase: Asset allocation becomes more crucial than factor selection.

By dynamically adjusting factor exposure based on economic conditions, investors can achieve consistent returns while managing risks effectively.

Can Passive Investing Alone Lead to Financial Freedom?

While passive investing offers low costs and simplicity, it may not be sufficient to achieve superior returns. Over the past decade, major indices have delivered modest annualized returns, with large-cap indices yielding less than 10% CAGR and mid-caps slightly outperforming at 12% CAGR. Factor investing provides an opportunity to enhance returns by strategically selecting outperforming factors.

Market Regime Shifts Determine Your Strategy

Market regimes shift over time due to changes in economic cycles, monetary policy, inflation trends, and investor sentiment. These shifts significantly influence the performance of various investment factors. For instance, during periods of economic expansion, momentum and small-cap factors tend to thrive as risk appetite increases and growth stocks outperform. Conversely, in times of economic slowdown or recession, quality and low-volatility factors provide resilience, helping investors preserve capital. Recognizing these shifts is crucial for factor investors, as rigidly adhering to a single-factor strategy may lead to underperformance in unfavorable market conditions.

Adaptive factor investing strategies offer a structured way to navigate different market environments while maintaining a disciplined approach. Multi-factor models, which combine factors such as value, quality, momentum, and low volatility, enable investors to capture opportunities across varying regimes. For example, in high-inflation environments, value stocks with strong earnings may outperform, while in a deflationary setting, growth-oriented factors could take the lead. Incorporating regime-aware factor investing ensures that portfolios remain resilient and responsive to changing market dynamics. By continuously monitoring macroeconomic indicators and factor trends, investors can tactically rebalance their portfolios, optimizing performance while minimizing drawdowns.

Conclusion: The Future of Smart Investing

At Wright Research, our research-driven multi-factor investment approach combines various factors to optimize risk-adjusted returns. Our actively managed multi-factor portfolios rebalance regularly and have demonstrated robust performance over the years. In 16 months since the launch of Wright PMS, we earned 80% returns for our clients – outperforming the benchmark by 45%.

Factor investing combined with quant is the smarter way to invest compared to traditional investing – we leverage data-driven insights and systematic strategies. By combining multiple factors dynamically, investors can create resilient portfolios that outperform over time. At Wright PMS, we remain committed to delivering consistent, risk-adjusted returns through our quant driven, factor-based investment philosophy.