Our view has remained “Extreme Caution” for more than 3 quarters primarily due to high valuations in most segments.

In most of the past monthly newsletters, we have mentioned the view of “Extreme Caution”. But we feel that the situation has now turned from bad to worse, because of the recent developments as mentioned ahead.

Reason 1: Business Cycle:

Business cycles are created due to economic growth, consumer demand, macroeconomic variables, monetary and fiscal policy or external shocks.

The overall risks in the system seem to suggest contraction of industrial activity as the business cycle seems to be peaking out in light of the dismal sales growth shown by most corporates for Q3.

Reason 2: High valuations in the Mid & Small Caps:

For the last 2 quarters, we have been mentioning the risk of overvaluation in the Midcaps & Small Caps.

In Sep, 2024 we mentioned “A flat or negative performance in Midcap or Small Cap sector for at least 3 months would ensure overall correction.”

The PEs for the Midcaps and Smallcaps remain elevated at 37.98 & 30.18 respectively.

As the rally of 2024 has been fueled by retail investors and SIPs in Mutual Funds, any adverse impact on Midcaps & Smallcaps is bound to impact the overall market.

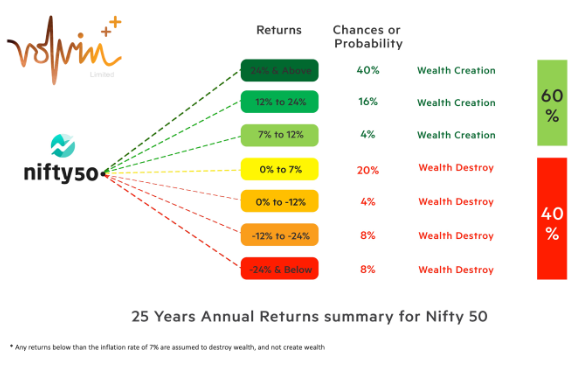

Reason 3: Nifty destroys wealth 40% of the time:

Past 25 years data suggests that 2 out every 5 years, Nifty does not create any wealth.

It would be unreasonable to expect markets to keep on going up without any correction.

Reason 4: Uncertain future due to reciprocal tariffs:

Reciprocal tariffs by US will ensure demand destruction for exporters. The domestic players could be hurt badly due to reduction in import duties.

Massive reduction in import duties for EVs will directly hit domestic automobile producers and disrupt the demand supply situation. The duty change was totally unexpected and a shock for the manufacturers who have planned massive capex.

Reason 5: China factor:

Due to massive housing crisis in China, it’s domestic demand is not as strong as previous years.

China’s strategy of bolstering its manufacturing sector through aggressive exports is creating significant challenges for businesses around the world especially in the steel, aluminum, and automobiles sectors.

Trump’s tariffs in combination with aggressive export stance of China could actually worsen the global trade by putting pricing pressure on other exporting countries, thus hitting their profitability much harder.

Reason 6: Increasing US Debt:

US debt has doubled in the last decade.

The debt is approximately US$ 36 trillion. The interest rates were between 1.0-1.5% in 2021. These have more than quadrupled in last 4 years.

Next few quarters are going to be extremely crucial for the Trump regime, as it will determine whether the tariffs will actually benefit the US economy or will hit inflation badly, as tariffs actually encourage inefficiencies by giving preference to high-cost domestic goods or services.

Reason 7: Muted Nifty Q3 earnings:

Nifty 50 profit growth consensus for the next year is around 10%. The current quarter earnings have not been up to the mark, clearly falling short of the double digit growth expectations.

With yoy growth reducing to around 5% for most companies, the current valuations seem to be high considering that equity risk premium is around 12-15%. Mid-caps and small caps, especially those corporates factoring in 15-20% growth for the next few years maybe severely hit going forward.

Nifty 16000?

No, we are not giving a target for Nifty!

Uncertainty due to US tariffs, aggression from Chinese exports, rising US debt have currently created higher risk in the system.

Also keeping in mind that

- Business cycle seems to be peaking out,

- Q3 results not living up to expectations,

- Nifty does not create wealth 40% of the time or every 2 out of 5 years,

- Excess supply situation due to high capacities impacts profitability more we feel it is more important to protect capital

Business sentiment slowdown not just impacts profits, but also affects market PE or sentiment.

The overvaluations in these very mid & small caps can ensure the slide for overall market as this rally was fuelled primarily due to investments by retail in in small and mid-caps.

With the current dismal Q3 numbers, there are chances of the forward earnings decreasing by 10%, rather than consensus 10% increase.

10% decrease in earnings translates into a forward PE of 23 for Nifty.

The average 20 PE for Nifty is made from highs of 24-26 and lows of 14-16.

We have seen in the past that Nifty PEs have gone to sub 16 levels whenever the slowdown is at its peak.

If the forward PE of 23 translates into current NIFTY of around 23000, a dismal scenario with a PE of 16 may translate into NIFTY 16000!